This guide explains how to choose between PPh Final 10% and PPh Badan 22% for your Bali villa (a frequently asked question among foreign property owners in Indonesia that can mean a difference of tens of millions of rupiah per year. The seo meta descriptions for this topic consistently rank among the highest-intent searches from expat villa owners across France, the UK, and Australia. Many foreign owners arrive in Bali believing they can apply the simpler PPh Final 10% flat rate on their gross rental income regardless of their legal structure. The reality is more nuanced: PT PMA and PT Lokal companies running operational villas are required to use PPh Badan 22% on net income, while individual owners and CV entities below Rp 50 billion in annual revenue may qualify for a flat final rate) and since PP 55/2022, eligible CVs can access a 0.5% rate for up to four years. Choosing the wrong regime does not only result in overpaying tax; it can trigger a DJP audit, reclassification, and penalties reaching 48% of the underpaid amount under UU KUP Article 13. This comprehensive guide covers the legal basis, comparative rate analysis, deductible expenses for PT PMA structures, three practical scenarios for French, UK, and Australian villa owners, and a compliance checklist to get your 2026 filing right.

What Is PPh Final Pasal 4(2) 10% and Who Can Apply It to a Bali Villa?

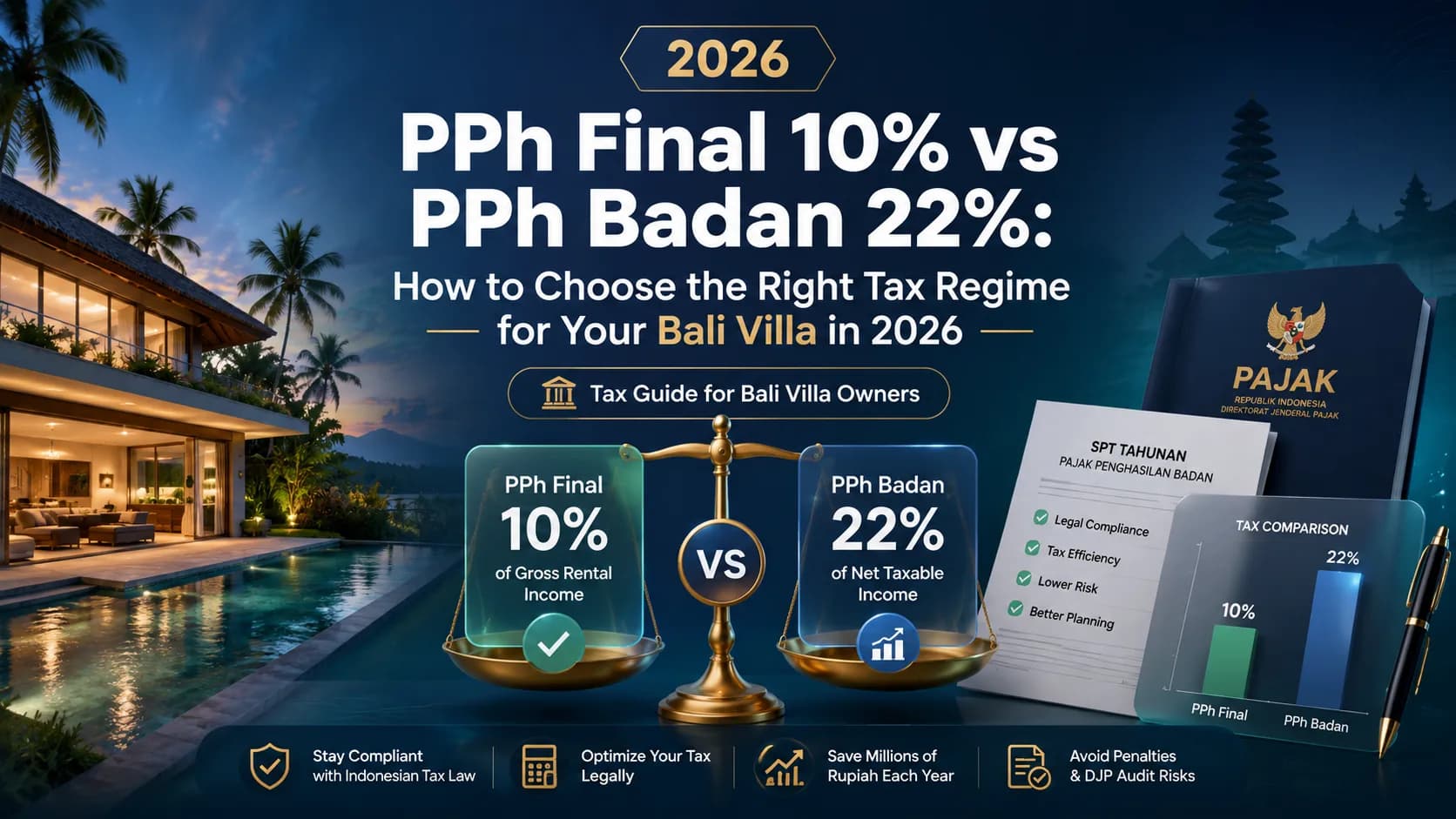

PPh Final under Pasal 4(2) of the Indonesian Income Tax Law (UU PPh) is a final withholding tax of 10% applied to gross rental income from land and buildings (sewa tanah dan bangunan). The word "final" means this tax extinguishes all further income tax liability on that income; it is not credited against any annual corporate tax calculation. This makes the administration simple: the tenant or OTA platform withholds 10% at source, and the villa owner has no further obligation to declare that income in a standard SPT.

Who Qualifies for PPh Final 10% on Villa Rental Income?

The regime is available to two categories of taxpayer under Indonesian law:

Individuals (Orang Pribadi): A French, UK, or Australian citizen who owns a Bali villa in their personal name and rents it out passively (meaning without maintaining operational staff, running a business entity, or providing hotel-like services) can apply PPh Final 10% on gross rental receipts. The income is classified as sewa tanah/bangunan under Pasal 4(2), not as business income under Pasal 4(1).

CV (Commanditaire Vennootschap) with revenue below Rp 50 billion: A CV operating a villa at a small scale (and crucially, eligible for the PP 55/2022 final tax regime) can elect 0.5% PPh Final on gross revenue for a maximum of four fiscal years, after which standard PPh Badan at 22% applies.

What PPh Final 10% Does Not Apply To

PPh Final 10% on sewa tanah/bangunan is explicitly unavailable to PT PMA and PT Lokal companies whose villa operations are classified as a business (usaha perhotelan) under KBLI 55194 or similar. The DJP consistently classifies villas managed through OTA platforms with operational staff as commercial hotel-like businesses, not passive rental of land and buildings. Applying PPh Final 10% to a PT PMA villa operation is one of the most common and costly errors seen in DJP audits of foreign-owned villa structures in Bali.

Sources: PPh Pasal 26 and withholding overview, pajak.go.id | UU 7/2021 HPP, peraturan.bpk.go.id

What Is PPh Badan 22% and How Does It Apply to PT PMA Villa Operations?

PPh Badan is the Indonesian corporate income tax applied to the net taxable income (Penghasilan Kena Pajak, PKP) of a legal entity. Under UU 7/2021 (Undang-Undang Harmonisasi Peraturan Perpajakan), the standard corporate rate is 22% for fiscal years 2022 onwards.

For a PT PMA or PT Lokal operating a villa in Bali (with staff, OTA integrations, cleaning services, pool maintenance, and guest reception) the entity is classified as an operating business. Its tax base is therefore net income: gross rental revenue minus all deductible business expenses. This is fundamentally different from PPh Final, which applies to gross revenue with no deduction allowed.

Pasal 31E: The 11% Rate for Small PT PMA and PT Lokal

Under Pasal 31E of UU PPh, Indonesian corporate taxpayers with gross annual revenue not exceeding Rp 50 billion benefit from a 50% tax rate reduction on the first Rp 4.8 billion of taxable income. This effectively reduces the rate on that portion to 11% (50% × 22%). Taxable income above Rp 4.8 billion is taxed at the standard 22%.

For a PT PMA villa generating Rp 40 billion in annual revenue with Rp 20 billion in taxable income after deductions, Pasal 31E produces significant savings: Rp 4.8 billion taxed at 11% (Rp 528 million) plus Rp 15.2 billion taxed at 22% (Rp 3.344 billion), for a total of Rp 3.872 billion, compared to Rp 4.4 billion under the flat 22% rate.

Sources: UU 7/2021 HPP English summary, peraturan.bpk.go.id | Coretax DJP SPT 1771 filing guide, pajak.go.id

PPh Final 10% vs PPh Badan 22%: Full Comparison Table

The table below compares both regimes across all dimensions relevant to a Bali villa owner. Rates, deductibility, and compliance obligations differ significantly depending on the legal structure used.

Criteria | PPh Final 10%, Individual or CV | PPh Badan 22%, PT PMA or PT Lokal |

|---|---|---|

Legal basis | UU PPh Pasal 4(2) | UU PPh Pasal 17 + UU 7/2021 |

Tax rate | 10% on gross revenue | 22% on net taxable income (11% on first Rp 4.8B under Pasal 31E) |

Tax base | Gross rental receipts, no deductions allowed | Net income after all deductible business expenses |

Eligible entities | Individuals; CV ≤ Rp 50B (0.5% under PP 55/2022 for 4 years) | PT PMA, PT Lokal (any size) |

Deductible expenses | None | Staff salaries 100%, BPJS 100%, building depreciation 5%/year, OTA commissions, maintenance |

Double taxation risk | None (final tax extinguishes all liability) | None if applied correctly, but applying Final on top of Badan creates illegal double taxation |

Annual return | SPT 1771 Final (annual filing via Coretax) | SPT 1771 Badan (due 30 April via Coretax) |

Monthly instalment | None for passive rental | PPh 25 monthly instalment (due 15th of each month) |

PPN 11% obligation | Exempt if jasa perhotelan (PMK 70/2022) | Exempt if jasa perhotelan, same rule applies |

DJP audit risk | Low for genuine passive individual rental | High if Final applied incorrectly to PT PMA |

Suitable for | Small individual or CV villa, passive income | Operational villa business with staff and OTA distribution |

Sources: PMK 96/2023 deductible expenses, jdih.kemenkeu.go.id | PwC Indonesia Pocket Tax Book 2026

Why PT PMA and PT Lokal Villa Operations Cannot Use PPh Final 10%

This is the most critical point of this guide, and it is frequently misunderstood by foreign villa investors in Bali.

The Operational Classification Rule

When a PT PMA or PT Lokal company operates a villa (meaning it employs staff, manages OTA bookings, provides cleaning and concierge services, and conducts ongoing business activities) the DJP classifies this as a business activity (kegiatan usaha) under Pasal 4(1) of UU PPh. Business income under Pasal 4(1) is taxable as corporate income under PPh Badan. It does not qualify for the Pasal 4(2) PPh Final regime, which is reserved for passive sewa tanah/bangunan income received by individuals or qualifying small entities.

The test applied by DJP auditors is functional: if the company maintains BPJS-registered employees, files monthly salary withholding (PPh 21), holds OTA contracts, and issues e-Faktur for services rendered, it is conducting business, not passively renting property.

The Double Taxation Trap

The most damaging error seen in DJP audits of PT PMA villa structures is the simultaneous application of PPh Final 10% on gross rental receipts AND PPh Badan 22% on net income. This produces an effective combined rate that can reach 32% or higher. There is no legal basis for this combination under Indonesian tax law, and when it is discovered during an audit, the DJP will reassess the entire tax position, apply the correct Badan-only regime, and impose interest penalties of 1.81% per month (per KMK 14/MK/EF.2/2026 Pasal 13 ayat 2) on any underpaid amounts, plus potential penalties of 50–100% of the tax due.

Deductible Expenses Available to PT PMA Villa Operations

The financial advantage of the Badan regime for operational villas is the ability to deduct all genuine business expenses before calculating taxable income. Under PMK 96/2023, the following categories are fully deductible:

Staff salaries and wages: 100% deductible. For a villa with 10 staff at an average monthly salary of Rp 8 million, annual staff costs reach Rp 960 million, a significant reduction in taxable income.

BPJS contributions (employer portion): 100% deductible. BPJS Ketenagakerjaan and BPJS Kesehatan employer contributions on staff salaries are a deductible business expense.

Building depreciation: Under PP 58/2023, permanent building structures are depreciated at 5% per year using the straight-line method. On a villa worth Rp 5 billion, annual depreciation is Rp 250 million of tax-deductible expense.

OTA commissions: Booking.com, Airbnb, Agoda, and similar platform commissions (typically 15–20% of booking value) are 100% deductible as a cost of revenue.

Maintenance and repairs: Regular maintenance, pool servicing, landscaping, and repair costs are deductible as ordinary business expenses.

Professional fees: Accounting, legal, and tax advisory fees paid to registered practitioners are deductible.

Sources: PMK 96/2023, jdih.kemenkeu.go.id | PP 58/2023 depreciation rates, jdih.kemenkeu.go.id

CV vs PT PMA: When the 0.5% Final Rate Under PP 55/2022 Makes Sense

For foreign villa investors who do not require a PT PMA structure (typically because their ownership is via an Indonesian nominee arrangement through a CV, or because they fall below the PT PMA minimum capital threshold) the PP 55/2022 regime offers a highly attractive option during its four-year window.

The PP 55/2022 Regime: 0.5% on Gross Revenue for Four Years

PP 55/2022 extended the UMKM final tax regime to CVs (commanditaire vennootschappen) and other non-PT entities with annual gross revenue not exceeding Rp 50 billion. Under this regime, eligible entities pay 0.5% of gross revenue as their final income tax, with no further Badan liability.

The four-year clock runs from the first fiscal year in which the entity registers under PP 55/2022. For a CV that registered in 2022, the favourable rate expires after fiscal year 2025, with standard 22% PPh Badan applying from 2026 onwards.

For a CV generating Rp 40 billion in annual villa revenue, the comparison is stark:

PP 55/2022 (0.5%): Rp 200 million tax per year

PPh Badan 22% net (after Rp 20 billion deductions): Rp 4.4 billion per year

The four-year window under PP 55/2022 can therefore produce cumulative tax savings of over Rp 16 billion for a mid-sized villa CV.

When to Transition from CV to PT PMA

Once the PP 55/2022 window closes, a CV paying full 22% PPh Badan loses its structural advantage over a PT PMA. At that point, foreign investors with sufficient capital should evaluate whether the PT PMA structure (with its larger deductible base, ability to distribute dividends at treaty rates under P3B, and stronger legal standing for asset protection) produces a better after-tax outcome. VillaTax models this transition automatically based on your revenue, expense profile, and applicable DTA.

flowchart TD

A[Villa Owner: Choose Tax Regime] --> B{Legal Structure?}

B -->|Individual direct ownership| C[PPh Final 10 percent on gross rental - Pasal 4 2]

B -->|CV revenue below Rp 50B| D{PP 55/2022 window open?}

B -->|PT PMA or PT Lokal| E[PPh Badan 22 percent on net income only]

D -->|Yes - within 4 years| F[0.5 percent PPh Final on gross - CV UMKM regime]

D -->|No - window expired| G[22 percent PPh Badan on net income]

E --> H[Deduct staff - BPJS - depreciation - OTA commissions]

H --> I[File SPT 1771 Badan via Coretax by 30 April]

C --> J[Withholding agent deducts 10 percent at source - no annual Badan filing]

F --> K[File annual gross revenue declaration - no deductions]

style A fill:#c9a962,color:#0c0e14

style E fill:#10b981,color:#fff

style F fill:#10b981,color:#fff

style C fill:#3b82f6,color:#fff

Three Practical Scenarios: France, UK, and Australia

Scenario 1, French Citizen, PT PMA, Rp 5 Billion Annual Revenue

A French tax resident owns a four-bedroom villa in Seminyak through a PT PMA company. Annual gross rental revenue via Airbnb, Booking.com, and direct bookings totals Rp 5 billion. The PT PMA employs 8 staff and provides full hotel-like services.

Applicable regime: PPh Badan 22% on net income. PPh Final 10% is not applicable.

Deductible expenses:

Staff salaries (8 × Rp 8M × 12): Rp 768 million

BPJS employer contributions: Rp 77 million

Building depreciation (5%/year on Rp 3B building): Rp 150 million

OTA commissions (15% × Rp 5B): Rp 750 million

Maintenance and utilities: Rp 300 million

Total deductible: Rp 2.045 billion

Taxable income (PKP): Rp 5B − Rp 2.045B = Rp 2.955 billion

PPh Badan calculation (Pasal 31E applies, revenue ≤ Rp 50B):

First Rp 2.955B at 11% (Pasal 31E): Rp 325 million

Total PPh Badan: Rp 325 million

Compared to an incorrect PPh Final 10% calculation: Rp 5B × 10% = Rp 500 million. The correct Badan regime produces Rp 175 million in annual savings, while the incorrect double-application would produce Rp 825 million in combined liability.

Additionally, when the PT PMA distributes profits as dividends to the French shareholder, the France–Indonesia DTA (Article 10) reduces the withholding rate from 20% to 15%, providing a further reduction on the after-tax distribution. Full details on the DTA procedure are covered in our dedicated article onDTA and DGT form procedure for Bali villa owners.

Scenario 2, UK Citizen, CV Structure, Rp 40 Billion Revenue, PP 55/2022 Window

A UK tax resident co-owns a villa complex in Canggu through a CV registered in 2023, with annual gross revenue of Rp 40 billion. The CV elected the PP 55/2022 regime upon registration.

Applicable regime for 2023–2026: 0.5% PPh Final on gross revenue. Tax liability 2026: Rp 40B × 0.5% = Rp 200 million

From 2027 onwards: Standard PPh Badan 22% on net income applies. Assuming Rp 20 billion in deductible expenses, taxable income = Rp 20 billion. Pasal 31E does not apply (revenue > Rp 50B). PPh Badan = Rp 20B × 22% = Rp 4.4 billion per year.

The cumulative four-year savings under PP 55/2022 compared to immediate Badan taxation: approximately Rp 16.8 billion. This is a material structural advantage that should be factored into any villa investment decision made before 2026.

Scenario 3, Australian Citizen, Individual Direct Ownership, Rp 2 Billion Revenue

An Australian tax resident owns a villa in Ubud in their personal name, renting it out passively through a local property manager with no operational staff. Annual gross rental income is Rp 2 billion.

Applicable regime: PPh Final 10% on gross rental income (Pasal 4(2)). Tax liability: Rp 2B × 10% = Rp 200 million, withheld at source by the property manager.

No SPT Badan filing is required. The income is declared in the owner's annual SPT Orang Pribadi (Form 1770) if the owner holds an Indonesian NPWP. If the owner has no NPWP and is a pure non-resident, PPh 26 at 20% applies instead of the Final 10% regime, making NPWP registration a significant tax-saving step for long-term Bali villa investors.

VillaTax handles NPWP registration, PPh Final tracking, and OTA-sourced income reconciliation automatically for individual villa owners across all five supported languages.

Sources: PMK 112/2025 DTA procedure, pajak.go.id | PwC Indonesia Pocket Tax Book 2026

PPN 11%: Is Your Bali Villa Exempt?

PPN (Pajak Pertambahan Nilai (VAT at 11%) is a separate tax from PPh. Under PMK 70/2022, jasa perhotelan) hotel and accommodation services, is exempt from PPN. This exemption covers villa rentals where the primary service provided is accommodation, including standard cleaning, reception, and concierge services. The exemption applies regardless of whether the villa operates under individual, CV, PT Lokal, or PT PMA ownership, provided the activity is classified as jasa perhotelan under the applicable KBLI code.

However, if a villa operation provides services that go beyond accommodation (such as restaurant meals, event management, spa services billed separately, or transportation) those additional services may be subject to PPN 11%. For the accommodation portion specifically, the exemption under PMK 70/2022 continues to apply in 2026.

Note that PMK 131/2024 introduced a 12% PPN rate on luxury goods and services. Villas priced at a luxury segment may be assessed by DJP under this elevated rate if their room rates exceed the luxury threshold defined in the regulation. Tax advisors recommend monitoring DJP guidance on this point through 2026.

Sources: Coretax DJP SPT 1771 guide, pajak.go.id | jdih.kemenkeu.go.id PMK 131/2024

Step-by-Step: Compliance Checklist and Key Deadlines for 2026

Step 1: Determine Your Legal Structure and Applicable Regime

Before filing anything, confirm which regime applies to your specific situation. Use the decision tree above as a starting point, and verify with a registered Indonesian tax consultant (Konsultan Pajak).

Step 2: Register for NPWP and PKP if Required

Any PT PMA or PT Lokal must hold an NPWP (Nomor Pokok Wajib Pajak) and register as a PKP (Pengusaha Kena Pajak) if annual revenue exceeds Rp 4.8 billion. Individual villa owners benefit strongly from NPWP registration, which converts their PPh liability from PPh 26 (20%) to PPh Final 10%.

Step 3: Set Up Coretax Compliance

Since January 2025, all tax filings in Indonesia use the new Coretax DJP system. The legacy e-SPT software is no longer accepted. PT PMA and PT Lokal must file SPT 1771 Badan electronically via Coretax. Monthly PPh 25 instalments are due by the 15th of each month. Annual SPT Badan is due by 30 April of the following year.

Step 4: Maintain Deductible Expense Documentation

For PT PMA and PT Lokal, maintain complete documentation for all deductible expenses: salary slips (slip gaji), BPJS payment receipts, depreciation schedules, OTA commission statements, maintenance invoices, and professional service contracts. DJP auditors require original documentation for all deductions claimed.

Step 5: Monitor DTA Compliance for Dividend Distributions

If your PT PMA distributes dividends to a foreign shareholder, ensure the DGT-1 form and Certificate of Residence are in place before the distribution. See our companion article on DTA benefits and the DGT form procedure under PMK 112/2025 for the complete process.

Action | Deadline | Responsible Party |

|---|---|---|

Confirm applicable tax regime | Before first income receipt | Villa owner / tax advisor |

NPWP and PKP registration | Before revenue threshold crossed | PT PMA / individual |

Monthly PPh 25 instalment | 15th of each month | PT PMA / PT Lokal |

Monthly PPh 21 (staff withholding) | 10th of following month | PT PMA / PT Lokal |

Quarterly PPN return (if applicable) | End of following month | PKP entities only |

Annual SPT 1771 Badan (Coretax) | 30 April | PT PMA / PT Lokal |

Renew PP 55/2022 election | Annually, before fiscal year end | CV entities |

DGT form renewal for DTA dividends | Before each distribution | PT PMA shareholder |

VillaTax automates PPh 25 instalment calculations, tracks monthly withholding deadlines, and generates Coretax-ready SPT data across all your OTA bookings and property income sources.

FAQ : Frequently Asked Questions

Is PPh Final 10% applicable to a PT PMA villa operation in Bali in 2026?

No. PPh Final 10% under Pasal 4(2) is not available to PT PMA or PT Lokal companies running operational villa businesses. These entities are required to apply PPh Badan 22% on net taxable income. Applying PPh Final to a PT PMA villa operation is an audit trigger and can result in reclassification, back-taxes, and penalties of up to 48% of underpaid amounts.

What deductible expenses can a PT PMA villa claim against PPh Badan?

A PT PMA operational villa can deduct 100% of staff salaries and BPJS contributions, building depreciation at 5% per year, OTA commissions, maintenance and repair costs, professional fees, and other ordinary business expenses under PMK 96/2023. These deductions can reduce the taxable income base by 40–60% compared to gross revenue, making the effective Badan tax rate significantly lower than the nominal 22%.

Can a CV use the 0.5% PPh Final rate for a Bali villa in 2026?

Yes, if the CV registered under PP 55/2022 before the end of 2022 and has annual gross revenue not exceeding Rp 50 billion, it can apply the 0.5% rate for its remaining eligible years. CVs that registered in 2022 exhaust their four-year window after fiscal year 2025. From 2026, they revert to standard PPh Badan 22% on net income. Consult your tax advisor to confirm the registration date and remaining eligibility.

Is PPN 11% applicable to villa rental income in Bali?

No, for most standard villa operations. Jasa perhotelan (accommodation services including villa rentals) is exempt from PPN 11% under PMK 70/2022. This exemption applies regardless of the legal structure. However, ancillary services such as restaurant meals, spa treatments, and event management billed separately may be subject to PPN. The luxury PPN rate of 12% under PMK 131/2024 may apply to very high-end villa offerings, seek specific advice from a Konsultan Pajak if your nightly rates fall in the luxury segment.

When is the SPT 1771 Badan deadline for Coretax filing in 2026?

The annual SPT 1771 Badan must be filed via the Coretax DJP system by 30 April of the year following the fiscal year. For fiscal year 2025, the deadline is 30 April 2026. Monthly PPh 25 instalments are due by the 15th of each month throughout the year. The legacy e-SPT system is no longer accepted, all filings must go through Coretax as of January 2025.

What happens if I apply both PPh Final 10% and PPh Badan 22% to the same PT PMA villa income?

This double application is illegal under Indonesian tax law and will be corrected by the DJP during an audit. There is no regime under which both PPh Final and PPh Badan apply simultaneously to the same income stream. If discovered, the DJP will assess the correct single regime, calculate the tax difference, and impose monthly interest at 1.81% per month plus potential fraud penalties. Avoid this situation by confirming your regime with a registered Konsultan Pajak before filing.

Conclusion

Choosing the correct income tax regime for your Bali villa is not optional; it directly determines your annual tax liability and your compliance exposure under DJP audit. PT PMA and PT Lokal villa businesses must use PPh Badan 22% on net income, with full access to deductible expenses that can dramatically reduce the effective rate. Individual owners and eligible CVs may access PPh Final 10% or the 0.5% PP 55/2022 rate, but only within their respective eligibility boundaries.

Incorrect application of PPh Final 10% to a PT PMA structure remains one of the most common and costly errors seen in foreign villa ownership in Bali. Getting this right (and maintaining Coretax compliance throughout the year) is exactly what VillaTax is built for. The platform calculates your PPh automatically booking by booking, tracks your monthly PPh 25 instalments, and generates Coretax-ready SPT data across all OTA channels. Start with a free diagnostic at villa-tax.operium.store.