If you own a villa in Bali, one of the biggest sources of confusion is taxation. Between PBJT, income tax (PPh), withholding tax, and the new Coretax reporting system, many owners are unsure how much they actually owe and what their real obligations are. This guide breaks down every tax that applies to a Bali villa rental business in 2026, with real calculation examples in IDR, a comparison of tools that can help you stay compliant, and a step-by-step walkthrough for getting your numbers right the first time. We answer the question people actually type into Google: how much tax do I really pay on my Bali villa.

How Much Tax Does a Bali Villa Owner Actually Pay?

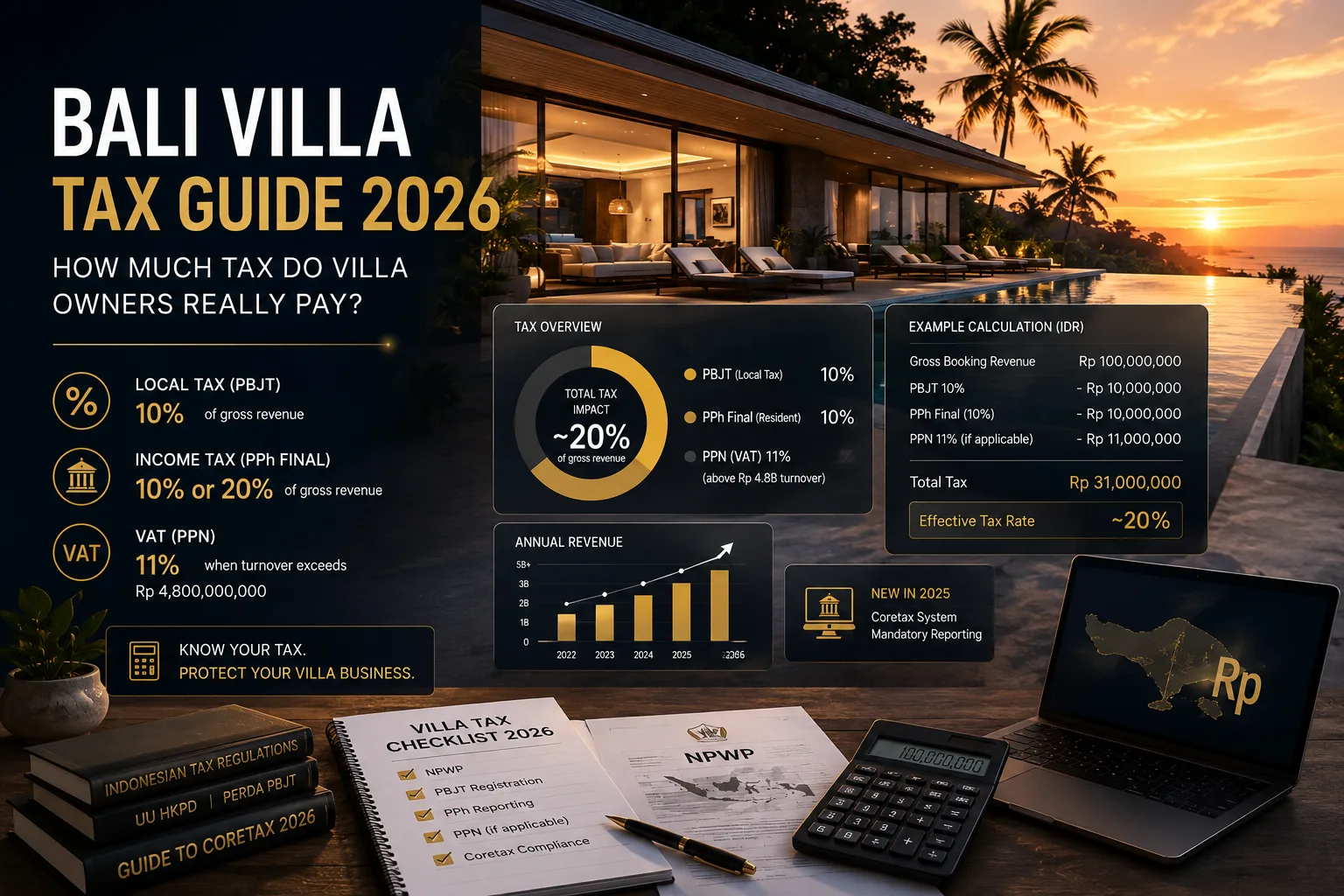

A Bali villa owner typically pays two layers of tax on rental income: a 10% local tourism tax (PBJT) collected from the guest, and a national income tax (PPh) calculated on the same gross revenue. For an individual Indonesian tax resident with an NPWP, PPh Final is 10% of gross revenue. For a foreign individual without Indonesian tax residency, PPh Final rises to 20%. For a PT PMA company structure, the applicable tax is PPh Badan at 25% of net profit instead of gross revenue. On top of this, PPN (VAT) at 11% becomes mandatory once annual turnover crosses Rp 4,800,000,000.

In practice, this means a resident owner renting out a villa typically loses around 20% of gross booking revenue to PBJT and PPh combined, before any operating costs. A non-resident owner without a double tax agreement benefit loses closer to 30%. Understanding which bracket you fall into is the single most important step before you can plan cash flow, pricing, or reinvestment.

The Three Layers of Bali Villa Taxation

Bali villa taxation is not a single tax — it is a stack of three distinct layers, each governed by a different authority:

Local tourism tax (PBJT) — collected by the regency (kabupaten) through Bapenda, the regional revenue agency

National income tax (PPh) — collected by DJP, the national tax office, through the Coretax system

National VAT (PPN) — collected by DJP once the turnover threshold is crossed

Each layer has its own filing calendar, its own forms, and its own penalty regime. A villa owner who only thinks about PBJT (because it appears on every Airbnb-style invoice) often misses the PPh obligation entirely, which is the layer most commonly missed and most heavily penalized during a DJP audit.

flowchart TD

A[Guest Books Villa] --> B[Gross Booking Revenue]

B --> C[PBJT 10 percent Local Tax]

B --> D[PPh Final 10 or 20 percent]

C --> E[Paid to Bapenda Regency]

D --> F[Paid to DJP via Coretax]

B --> G{Annual Revenue above Rp 4.8 Billion}

G -->|Yes| H[PPN 11 percent Applies]

G -->|No| I[No PPN Obligation]

style A fill:#c9a962,color:#0c0e14

style F fill:#10b981,color:#fff

What Taxes Apply to a Bali Villa Rental Business?

Depending on your ownership structure and operating model, several distinct taxes may apply simultaneously. Understanding the full list before you start operating — rather than discovering them one by one through penalty notices — is the difference between predictable cash flow and constant surprises.

PBJT — The Local Tourism and Accommodation Tax

PBJT (Pajak Barang dan Jasa Tertentu) is a regional tax that replaced several older local taxes under Indonesia's 2022 fiscal harmonization law (UU HKPD). For villa rentals classified as jasa perhotelan (hospitality services), PBJT is charged at 10% of the gross transaction value — meaning the full amount the guest pays, including cleaning fees and service charges in most regencies.

PBJT is collected from the guest at the point of payment and remitted by the villa operator to the local Bapenda office. It is a regency-level tax, which means the exact reporting portal, deadlines, and enforcement intensity vary between Badung, Gianyar, Denpasar, Buleleng, Tabanan, Klungkung, Bangli, Karangasem, and Jembrana. Badung — home to Seminyak, Canggu, Uluwatu, and the airport corridor — has the most mature digital reporting infrastructure and the most active enforcement team, simply because it has the highest concentration of villa rental activity in Bali.

PPh — National Income Tax on Rental Revenue

PPh (Pajak Penghasilan) is the national income tax layer, and its rate depends entirely on your tax residency status and legal structure:

Owner Status | Tax Rate | Tax Base |

|---|---|---|

Indonesian tax resident (NPWP) | 10% | Gross rental revenue |

Foreign non-resident, no DTA benefit | 20% | Gross rental revenue |

Foreign non-resident with applicable DTA | 10% in most real cases | Gross rental revenue |

PT PMA company | 25% | Net profit (not gross) |

This is where most confusion happens. Many foreign owners assume that having a double tax agreement (DTA / P3B) between Indonesia and their home country automatically reduces their rate to the treaty's standard withholding percentage. In reality, rental income from real estate located in Indonesia almost always falls under Article 6 of the OECD Model Convention, which most Indonesian DTAs follow. Article 6 grants the taxing right to the country where the property is physically located — Indonesia — regardless of the treaty's general withholding article. This means villa rental income is taxed in Indonesia at the standard non-resident rate of 20% in the vast majority of real configurations, not at a reduced treaty rate. Owners who assume otherwise frequently underpay and face penalties during reconciliation.

PPh Badan — Corporate Income Tax for PT PMA Structures

If your villa is held through a PT PMA (a foreign-owned limited liability company), the taxation model changes completely. Instead of a flat percentage on gross revenue, PT PMA structures pay PPh Badan at 25% on net profit — meaning gross revenue minus deductible operating expenses (maintenance, staff salaries, management fees, depreciation, marketing). This can be significantly more favorable than the 20% non-resident individual rate if your operating costs are substantial, because the tax base shrinks accordingly. It can also be less favorable for a villa with very low operating costs and high margins, because 25% of a larger net figure can exceed 20% of gross.

PPN — Value Added Tax Above the Threshold

PPN (Pajak Pertambahan Nilai) at 11% becomes mandatory once your business — whether an individual or a PT PMA — crosses Rp 4,800,000,000 in annual turnover. At that point you must register as a PKP (Pengusaha Kena Pajak — a VAT-registered business) and begin charging PPN on top of your rental rates, filing monthly VAT returns, and reconciling input versus output VAT. This threshold catches multi-villa operators and larger single-property luxury villas faster than most owners expect, especially in high-season months where a single villa can generate Rp 400-600 million.

Other Taxes Bali Villa Owners Frequently Encounter

Beyond the three core layers above, several other taxes apply at specific moments in a villa's lifecycle:

PBB (Pajak Bumi dan Bangunan) — annual property tax of 0.1% to 0.5% of the NJOP (assessed tax value) of the land and building, paid yearly regardless of rental activity

BPHTB (Bea Perolehan Hak atas Tanah dan Bangunan) — a one-time 5% tax on the purchase price, paid by the buyer at acquisition

PPh on sale — when a villa is sold, the seller typically pays 2.5% of the transaction value as a final income tax

PPN on new construction — 11-12% applies to new-build construction contracts in many configurations

Luxury property surtax — an additional 10-20% can apply to villas valued above approximately Rp 30 billion

Example: Villa Generating IDR 100 Million Per Month

Concrete numbers make the abstract tax stack much easier to understand. Let's walk through a realistic villa generating Rp 100,000,000 in gross monthly revenue, which corresponds to a well-positioned 3-bedroom villa in Canggu or Ubud running at a healthy occupancy rate.

Scenario A — Indonesian Tax Resident Individual (NPWP)

Line Item | Calculation | Amount (IDR) |

|---|---|---|

Gross monthly revenue | — | 100,000,000 |

PBJT (10%) | 100,000,000 × 10% | 10,000,000 |

PPh Final resident (10%) | 100,000,000 × 10% | 10,000,000 |

Total tax burden | PBJT + PPh | 20,000,000 |

Net revenue after tax | 100,000,000 − 20,000,000 | 80,000,000 |

A resident owner keeps approximately 80% of gross booking revenue before operating costs (staff, maintenance, utilities, OTA commissions) are deducted.

Scenario B — Foreign Non-Resident Individual, No DTA Benefit (Standard Real-World Case)

Line Item | Calculation | Amount (IDR) |

|---|---|---|

Gross monthly revenue | — | 100,000,000 |

PBJT (10%) | 100,000,000 × 10% | 10,000,000 |

PPh Final non-resident (20%) | 100,000,000 × 20% | 20,000,000 |

Total tax burden | PBJT + PPh | 30,000,000 |

Net revenue after tax | 100,000,000 − 30,000,000 | 70,000,000 |

This is the most common real-world scenario for foreign individuals who own a villa personally (rather than through a PT PMA) and who incorrectly assumed their home country's DTA would reduce this rate — see the Article 6 explanation above.

Scenario C — PT PMA Company Structure

Line Item | Calculation | Amount (IDR) |

|---|---|---|

Gross monthly revenue | — | 100,000,000 |

PBJT (10%) | 100,000,000 × 10% | 10,000,000 |

Estimated operating costs | ~35% of gross (staff, maintenance, utilities, OTA fees) | 35,000,000 |

Net profit before PPh Badan | 100,000,000 − 35,000,000 | 65,000,000 |

PPh Badan (25%) | 65,000,000 × 25% | 16,250,000 |

Total tax burden | PBJT + PPh Badan | 26,250,000 |

Net revenue after tax | 100,000,000 − 26,250,000 | 73,750,000 |

In this example, the PT PMA structure lands between the resident individual scenario and the non-resident individual scenario, because operating costs reduce the taxable base before the 25% rate applies. The exact outcome depends heavily on how much of the 35% operating cost assumption holds true for your specific property — villas with in-house staff, pools, and gardens typically run higher overhead than minimalist studios.

For a quick way to estimate your own villa's tax burden across all three scenarios without manual spreadsheet work, VillaTax's audit tool calculates this automatically based on your actual booking history and ownership structure.

PBJT for Villa Operators: What You Actually Need to Know

PBJT replaced several older, fragmented local taxes (including the previous hotel and restaurant tax framework) and is now the single most consistent compliance requirement for villa operators across all nine Bali regencies. Despite its apparent simplicity — a flat 10% — the practical mechanics trip up a significant number of owners every year.

Who Has to Collect PBJT?

Any villa, guesthouse, or short-term rental property operating as jasa perhotelan must collect PBJT on every paid booking, regardless of whether the booking originated from a direct website inquiry, WhatsApp, Airbnb, Booking.com, Traveloka, Agoda, or any of the 300+ other platforms now connected to villa distribution in Bali. The obligation to collect and remit PBJT sits with the property operator — not with the OTA — even when the OTA itself charges its own service fee on top of the booking.

Common PBJT Mistakes

The single most expensive misunderstanding in Bali villa taxation is assuming that Airbnb, Booking.com, or other platforms already handle PBJT on the owner's behalf. They do not. OTAs collect their own commission and, in some cases, their own VAT obligations in their home jurisdiction — none of this satisfies the Indonesian PBJT obligation, which remains entirely the villa operator's responsibility to calculate, collect, and remit to the regency's Bapenda.

A second frequent mistake is calculating PBJT on net revenue (after OTA commission) instead of gross revenue (the full amount the guest paid). PBJT must be calculated on the gross transaction value charged to the guest, before any platform commission is deducted on the operator's side.

A third mistake is missing the monthly SPTPD (Surat Pemberitahuan Pajak Daerah) filing deadline. Most Bali regencies require monthly PBJT reporting, and late filing triggers an administrative penalty even when the underlying tax was eventually paid correctly — the lateness itself is sanctioned independently of the tax amount.

Failure to Collect or Report PBJT Correctly

Failure to collect or report PBJT correctly can result in penalties calculated as a percentage of the unpaid or late-paid tax, plus monthly compounding interest, applied retroactively from the original due date. In a regency audit, Bapenda officers cross-reference OTA booking data (increasingly available through data-sharing arrangements) against the villa's declared PBJT filings. A gap between actual booking volume and declared revenue is the single most common trigger for a regency-level tax investigation in Bali's tourism corridor.

"Villa owners who treat PBJT as an afterthought rather than a monthly discipline are the ones who end up facing multi-year retroactive assessments when a regency audit eventually catches the gap." — Common pattern observed across Bali regency compliance reviews

Coretax and Reporting Requirements

Indonesia's Coretax system, rolled out progressively by the Direktorat Jenderal Pajak (DJP) starting in 2024 and now fully operational across the national tax administration, is fundamentally changing how income tax reporting and compliance are managed for every taxpayer in the country — including Bali villa owners.

What Coretax Changes for Villa Owners

Coretax consolidates a taxpayer's entire fiscal profile — NPWP registration, income declarations, withholding records, and payment history — into a single integrated digital system. For villa owners, the practical implication is that DJP now has dramatically improved visibility into cross-referencing income reported through various channels, including data increasingly obtained from financial institutions, payment processors, and in some cases platform-level reporting arrangements.

This means the gap between what a villa actually earns (visible through OTA booking platforms, payment gateway records, and bank deposits) and what gets declared through SPT Tahunan (the annual tax return) is far easier for DJP to detect than it was under the previous, more fragmented reporting infrastructure.

Coretax Reporting Requirements for Villa Operators

Villa owners should ensure that:

Revenue is accurately recorded across every booking channel, including direct bookings that bypass OTAs entirely

OTA bookings are reconciled monthly against actual bank deposits, accounting for currency conversion when payouts arrive in USD or EUR and must be converted at the official DJP Kurs Pajak (weekly tax exchange rate) rather than the rate your bank happened to apply

Tax reports are submitted correctly and on time, including both the monthly PPh withholding-style filings where applicable and the annual SPT Tahunan

Supporting documentation is available — booking confirmations, payment records, and reconciliation logs — in case of a Coretax-triggered information request

Practical Coretax Compliance Workflow

flowchart TD

A[Booking Received on Any Channel] --> B[Record Gross Revenue in IDR]

B --> C[Apply DJP Kurs Pajak if Foreign Currency]

C --> D[Calculate PBJT 10 percent]

C --> E[Calculate PPh Based on Residency Status]

D --> F[File Monthly SPTPD with Bapenda]

E --> G[Reconcile via Coretax System]

G --> H[File Annual SPT Tahunan]

style A fill:#c9a962,color:#0c0e14

style G fill:#10b981,color:#fff

The villas that handle this transition most smoothly are the ones that already maintain clean, channel-by-channel revenue records before a Coretax-triggered request ever arrives — reconstructing a full year of OTA-by-OTA revenue retroactively, under time pressure, is a far more stressful and error-prone process than maintaining the records proactively each month. Tools like VillaTax automate this reconciliation by pulling booking data directly from 310+ connected OTA platforms via webhook, iCal sync, or email parsing, then applying the correct PBJT and PPh calculation automatically per booking.

Common Mistakes Villa Owners Make

Across hundreds of villa tax situations in Bali, the same handful of mistakes account for the overwhelming majority of penalty notices and retroactive assessments. Recognizing these patterns early is far cheaper than discovering them during an audit.

1. Assuming OTA Taxes Cover All Obligations

Airbnb, Booking.com, and similar platforms may charge their own service fees, and in some jurisdictions collect local occupancy taxes on the platform's behalf — but none of these mechanisms satisfy Indonesia's PBJT or PPh obligations. These remain entirely separate, entirely the operator's responsibility, and entirely unaffected by whatever the OTA itself does on its own platform fee.

2. Mixing Personal and Business Revenue

Owners who run villa rental income through a personal bank account alongside unrelated personal transactions make their own reconciliation dramatically harder and raise red flags during any DJP review, since the agency cannot easily distinguish business revenue from personal transfers, gifts, or unrelated income in a mixed account.

3. Missing PBJT Reporting Deadlines

Most regencies require monthly SPTPD filing. A villa owner who files quarterly, annually, or "whenever I remember" accumulates late-filing penalties independently of whether the underlying tax amount was ultimately correct.

4. Not Reconciling Airbnb and Booking.com Transactions

Platform payout reports rarely match gross booking value line-by-line — commissions, currency conversion, cancellations, and refunds all create discrepancies between what a guest paid and what hits the owner's bank account. Reconciling at the payout level instead of the booking level routinely produces incorrect PBJT and PPh calculations, because both taxes must be calculated on the gross booking amount, not the net payout received after OTA commission.

5. Using Spreadsheets That Cannot Support an Audit

A spreadsheet that only shows monthly totals — with no booking-by-booking traceability back to the original OTA transaction, guest name, and payment date — collapses under audit scrutiny. DJP and Bapenda officers expect to see a clear trail from individual booking to tax calculation to filing. Systems purpose-built for Bali villa tax compliance, rather than generic spreadsheets, maintain this traceability automatically.

How to Calculate Your Bali Villa Taxes: Step-by-Step Guide

The exact calculation depends on four variables: your ownership structure, your revenue level, your property's location (regency), and the type of guest accommodation service you provide. Here is the practical, repeatable process.

Step 1: Determine Your Tax Residency and Legal Structure

Establish whether you are an Indonesian tax resident with an NPWP, a foreign individual without Indonesian tax residency, or operating through a PT PMA. This single decision determines whether your PPh rate is 10%, 20%, or 25% on a different tax base entirely (net profit instead of gross revenue for PT PMA).

Step 2: Identify Your Regency and Confirm the Local PBJT Rate

While 10% is the standard PBJT rate applied to tourism accommodation services across Bali's regencies, always confirm the specific Perda (local regulation) for your regency — Badung, Gianyar, Denpasar, Buleleng, Tabanan, Klungkung, Bangli, Karangasem, or Jembrana — since reporting portals and minor procedural requirements differ.

Step 3: Consolidate Revenue Across Every Booking Channel

Gather gross booking revenue from direct bookings, your own website, WhatsApp inquiries, and every connected OTA — Airbnb, Booking.com, Agoda, Traveloka, Tiket, Expedia, Vrbo, and others. Convert any foreign-currency payouts to IDR using the official weekly DJP Kurs Pajak rate, not your bank's spot rate.

Step 4: Apply PBJT to Gross Revenue

Calculate 10% of the full gross transaction value (what the guest paid, including service fees in most regencies) for every booking, regardless of channel.

Step 5: Apply the Correct PPh Rate to the Correct Base

Apply 10% (resident) or 20% (non-resident, standard real-world case) to gross revenue, or apply 25% to net profit after deductible expenses if operating through a PT PMA.

Step 6: Check the PPN Threshold

If your trailing twelve-month revenue is approaching or has crossed Rp 4,800,000,000, begin the PKP registration process and start applying PPN at 11% going forward.

Step 7: File Monthly PBJT (SPTPD) and Reconcile via Coretax

Submit your monthly local tax filing to Bapenda and ensure your income figures are correctly reflected for the annual SPT Tahunan filed through Coretax.

Step 8: Maintain Booking-Level Documentation

Keep a permanent, exportable record linking every booking to its tax calculation, in case of a future audit request from either Bapenda or DJP.

Comparing Your Options: Manual Process vs Dedicated Tax Software

Criteria | Manual Spreadsheet | Generic Accounting Software | VillaTax |

|---|---|---|---|

PBJT auto-calculation per booking | No | No | Yes |

PPh rate by residency status | Manual lookup | No | Automatic |

OTA import (300+ platforms) | No | Limited | Yes, webhook + iCal + email parser |

DJP Kurs Pajak auto-conversion | Manual | No | Automatic weekly update |

Coretax-ready export | No | Generic only | Purpose-built |

Multi-regency Perda awareness | No | No | Yes |

Audit-ready booking trail | Manual effort | Partial | Built-in |

Legal compliance shield | None | None | PT Asiah Legal Jaya Compliance Shield |

Languages | N/A | Usually 1 | 5 (EN/FR/DE/ES/ID) |

Using dedicated software built specifically around Indonesian villa taxation can significantly reduce reporting errors and compliance risk compared to spreadsheets or generic accounting tools designed for other markets. VillaTax's pricing page outlines the available plans for individual owners, multi-villa portfolios, and agencies managing properties on behalf of multiple investors.

What Happens If You Get It Wrong: Penalty Mechanics

Both PBJT and PPh penalty regimes follow similar logic: a percentage-based surcharge on the unpaid or underpaid tax, plus monthly compounding interest calculated from the original due date until the date of actual payment. In practice, this means a discrepancy left uncorrected for 12-18 months can grow substantially beyond the original tax gap, since interest compounds month over month rather than applying as a single flat penalty.

DJP's Coretax-era cross-referencing capability, combined with Bapenda's increasing access to OTA-level booking data, means the detection window for discrepancies has shortened considerably compared to five years ago. Owners who assumed a gap would simply go unnoticed indefinitely are increasingly finding that assumption tested during routine compliance reviews rather than only during targeted audits.

This section also doubles as a quick reference for seo meta descriptions and search snippets, since each answer below is written as a self-contained, quotable explanation of how to handle a specific Bali villa tax situation.

FAQ — Frequently Asked Questions

How much tax do I pay on a Bali villa as a foreign owner?

As a foreign individual owner without Indonesian tax residency, you typically pay 10% PBJT plus 20% PPh Final on gross rental revenue, for a combined tax burden of approximately 30%, since most double tax agreements do not reduce this rate for real estate income under Article 6 of the OECD Model Convention.

Does my country's double tax agreement reduce my Bali villa tax rate?

In almost all real-world cases, no. Rental income from real estate is taxed in the country where the property is located under Article 6 of most DTAs, which means Indonesia retains full taxing rights regardless of your home country's treaty with Indonesia, and the standard 20% non-resident PPh rate applies.

What is PBJT and who has to pay it?

PBJT (Pajak Barang dan Jasa Tertentu) is a 10% local tourism tax charged on accommodation services in Bali, collected from the guest at the time of payment and remitted by the villa operator to the regency's Bapenda office, regardless of which booking channel was used.

Does Airbnb or Booking.com pay my Bali villa taxes for me?

No. OTA platforms charge their own commissions and may collect certain taxes for their own jurisdiction, but none of this satisfies Indonesia's PBJT or PPh obligations, which remain entirely the responsibility of the villa operator to calculate, collect, and remit.

How is PPh calculated for a PT PMA-owned villa?

A PT PMA pays PPh Badan at 25% on net profit (gross revenue minus deductible operating expenses), rather than a flat percentage on gross revenue as applies to individual owners, which can be more or less favorable depending on your actual operating cost ratio.

When do I need to register for PPN on my Bali villa?

PPN registration as a PKP becomes mandatory once your trailing twelve-month gross turnover crosses Rp 4,800,000,000, at which point you must begin charging 11% VAT and filing monthly VAT returns.

What happens if I underpaid PBJT for several years without realizing it?

You face a retroactive assessment covering the underpaid amount plus a percentage-based penalty and monthly compounding interest calculated from each original due date, which is why proactive monthly reconciliation is significantly cheaper than a multi-year correction discovered during an audit.

Can I calculate my Bali villa taxes myself with a spreadsheet?

Yes, technically, but spreadsheets struggle to maintain booking-level traceability across hundreds of transactions from multiple OTA channels with different currencies and commission structures, which is precisely the level of detail that an audit typically requires.

What is Coretax and why does it matter for villa owners?

Coretax is DJP's integrated national tax administration system, rolled out from 2024 onward, which consolidates a taxpayer's full fiscal profile and dramatically improves the tax office's ability to cross-reference declared income against actual financial activity, making accurate and timely reporting more important than ever for villa owners.

Is there a free tool to estimate my Bali villa tax burden?

You can run a free, automated audit of your villa's compliance status — including an estimated tax gap analysis — through VillaTax's audit tool, which connects to your booking history and calculates PBJT and PPh exposure automatically.

Final Thoughts

The cost of non-compliance in Bali's villa rental market is almost always higher than the tax itself once penalties, compounding interest, and the operational disruption of an audit are factored in. Villa owners — whether individual residents, foreign non-residents, or PT PMA structures — should understand their specific obligations early, reconcile revenue monthly rather than annually, and implement a proper booking-to-tax-calculation trail before issues arise rather than after a regency or DJP notice lands.

For owners who want to move from manual spreadsheets to an automated, audit-ready system built specifically for Bali's nine regencies and Indonesia's national tax framework, VillaTax connects directly to 310+ booking platforms, applies the correct PBJT and PPh calculation per booking, and keeps your records Coretax-ready year-round. Explore the pricing plans or run a free compliance audit to see exactly where your villa stands today.